How to set the perfect budget target

Control charts are the tool you didn’t know you needed

The 4 years I lived in San Francisco were the most financially reckless years of my life. They were also the most fun.

Even as I spent nearly every dollar I made on a whimsical Peter Pan lifestyle, I was still an avid budgeter through it all.

The problem was that I didn’t value saving, and because of that, there was nothing to stop me from setting my spending targets absurdly high. Sticking to a budget is easy when your spending limits are in the stratosphere.

A string of back-to-back layoffs would eventually wake me up to the pain and desperation that come from not having financial reserves, and within a year, I became a born-again saver.

I made it my mission to never again be so financially frail and vulnerable. It was from that place that I stumbled across the hands-down best way to set and track my spending targets.

The law of spending

If you’re serious about budgeting, your behavior is highly influenced by how you set your spending targets. This was true even on my most financially hedonistic days.

The world of economics has something called Parkinson’s Law, which states that “work expands so as to fill the time available for its completion.” In other words, if you have a week to get something done, it’ll take a week to do.

This law also applies to our budgets: your spending always rises to the limit you set.

This is why it’s important to have a plan that accounts for both savings and lifestyle.

Saving through spending

Saving was the first and hardest skill I had to learn when I finally snapped out of my delusion and started growing up. Your ability to save rests on how you set your spending levels.

As a new saver, the highest hurdle to overcome is facing what seems like an impossibly long savings timeline. If you can’t see yourself ever reaching the top of the mountain, you’re unlikely to start climbing in the first place.

Building some initial savings quickly is how you overcome that first barrier and start climbing the savings mountain. Successfully getting some savings under your belt provides potent evidence that you’re actually capable of saving.

You begin to believe you can do it, and that belief is what keeps you putting one foot in front of the next. In the beginning, your self-confidence and mindset are of paramount importance.

While you may want to build this early savings as fast as humanly possible, there’s a delicate balance to strike.

If you’re too aggressive and give yourself a spending allowance that’s too low, you’ll inevitably overspend and lose confidence in your ability to change your ways.

If you’re not aggressive enough, however, and give yourself too generous a spending allowance, then you lose the ability to quickly build that crucial initial savings. Summiting Mt. Savings starts looking impossible again.

The key is to set your spending levels just right.

A clue from work

Figuring out a ‘goldilocks’ range is a common problem in business and, because of that, there’s a vast body of knowledge dedicated to understanding when processes are running within a normal range.

Exposure to problems like this at work is how I became acquainted with the humble, but powerful, control chart.

In the deep world of Quality Management (i.e. Six Sigma and LEAN manufacturing), control charts are a foundational tool used to detect when a process is going haywire.

Things clicked for me when I realized that my day-to-day spending patterns closely resembled the data and trends I was seeing at work. If I could spend 8 hours a day explaining normal ranges to execs, why couldn’t I do the same with my spending?

Why we pick the wrong targets

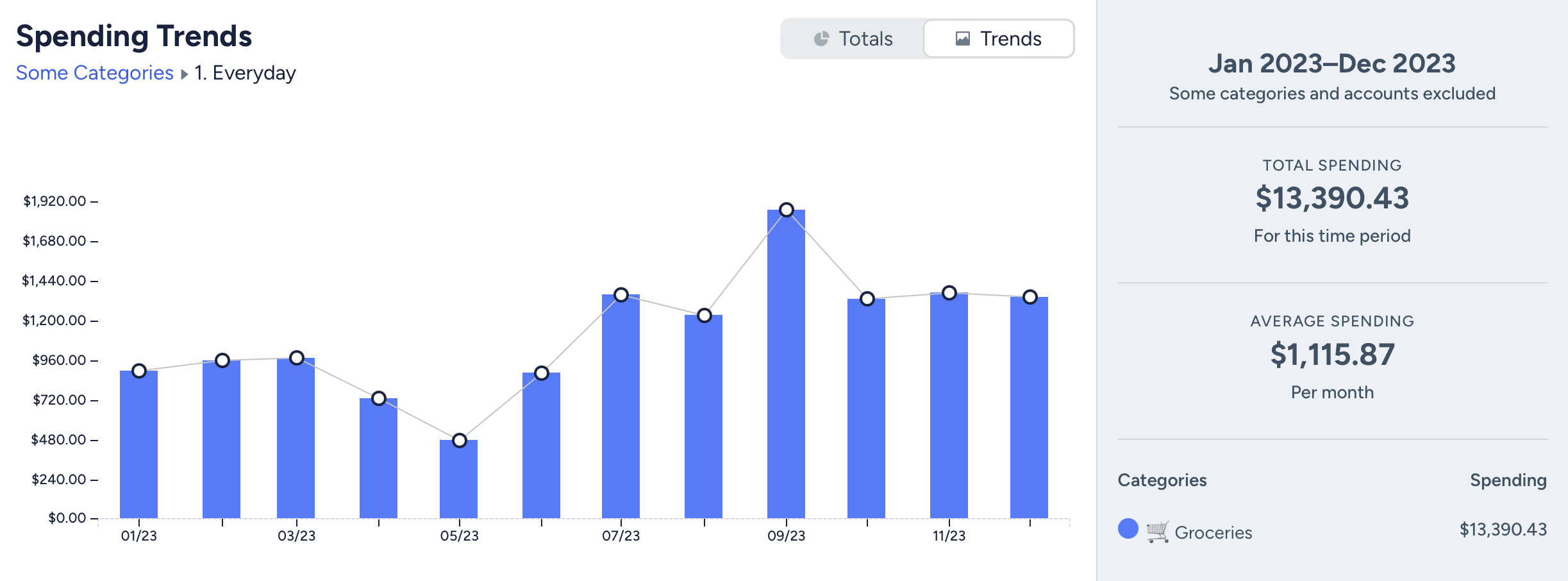

YNAB, my budgeting app of choice, is wonderful for tracking your spending and helping you stick to a spending plan. But it’s up to you to decide the plan.

The mistakes I made in choosing targets were informed by YNAB’s basic Reporting tab. I’ve recreated that chart below using dummy data to show you what I mean.

I was basically eyeballing it. Doing my best to determine if I should use the short bars, the tall bars, or the average.

Your friend the control chart

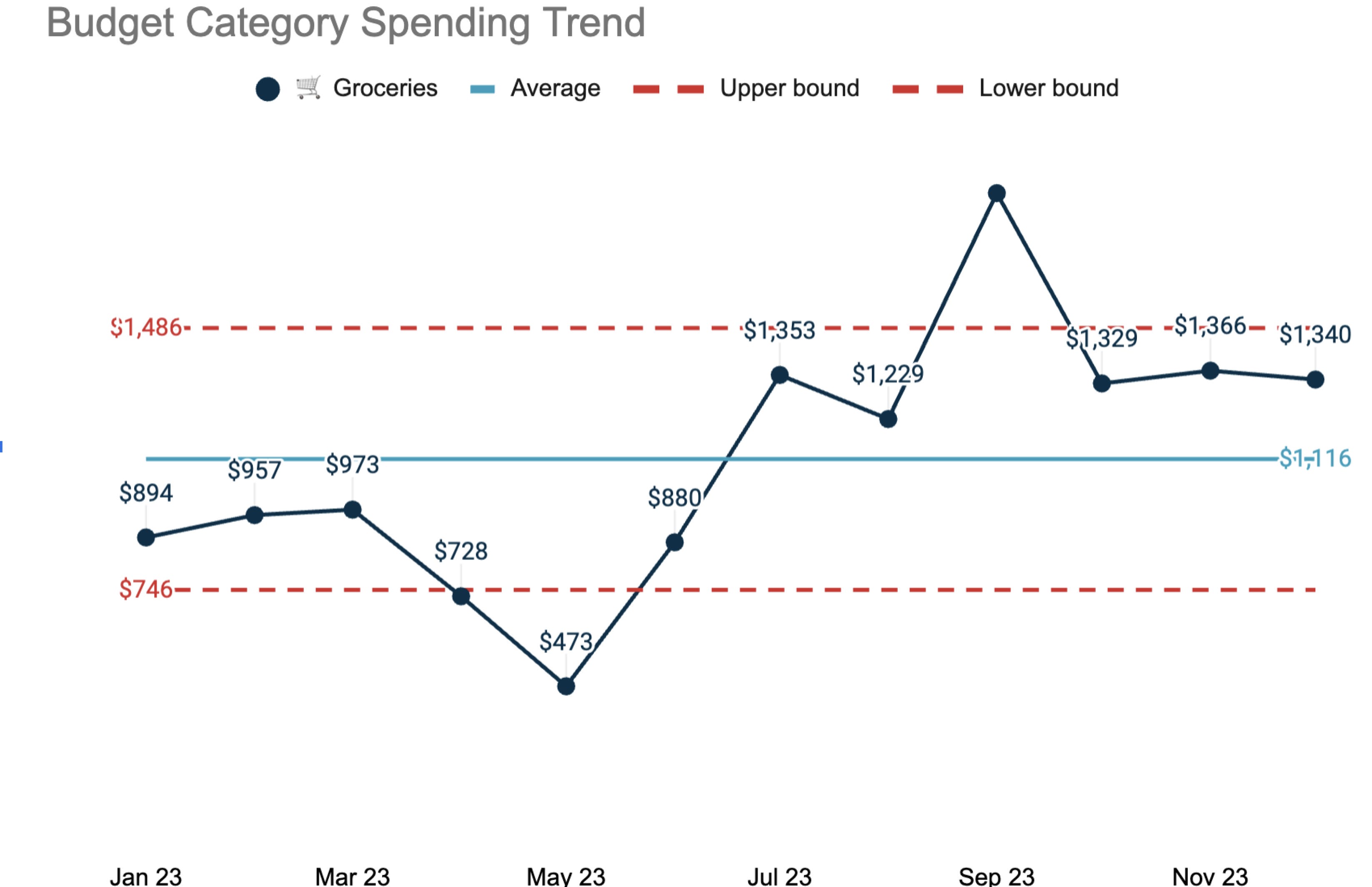

Here’s how the same dummy data in the graph above looks through a control chart I’ve adapted for personal finance use.

For a given budget category, the black line tells the story of how your spending shifts from one month to the next. The bar chart from before gave us that, but the control chart contextualizes the information.

The solid blue line represents the average spending, and the dotted red lines represent the upper and lower bounds. Without boring you with a bunch of math, any spending that falls between these dotted lines is considered normal.

If you have a particularly expensive month, you don’t have to automatically freak out. You can instead ask if it fell above the upper bound. November’s $1,366 was high, but it was on the high end of the normal range. No reason to sound the alarm.

More importantly however, seeing the normal range allows you to intelligently select spending targets based your goals.

If you're trying to quickly build savings, it might be tempting to try to repeat your most frugal month (you’ve done it before right?). But this is where you could unwittingly set yourself up for failure.

Digging into the data for May, you’d see that the $473 grocery figure was low because you were out of town on a vacation, so it’s unreasonable to expect your grocery budget to look like that on a typical month at home.

Control chart to the rescue. Setting your spending limit to the lower bound of the normal range ($746) ensures that you’re still lowering your spending limit, but in a way that’s realistic and sustainable over the long run.

Why they work

As you can see, the magic of the control chart comes from those dotted lines. They’re calculated from the spending data itself using its standard deviation.

Though the name sounds scary, standard deviation is simply a common way of measuring how far, on average, each data point falls from the average.

The wackier your spending, the bigger the standard deviation. The more predictable your spending, the smaller your standard deviation. The upper and lower bounds are just the average plus and minus the standard deviation.

These average, upper, and lower bounds are dynamic, meaning that each month they’re recalculated. So if your life changes in a big way (like when you move to a new city) they’ll automatically adjust.

Control charts give you a fantastically precise and nuanced view of your spending that allows you to:

Build forecasts using data-informed assumptions

Easily detect outliers, and react to them accordingly

Pick sustainably low and conservatively high spending targets

See the seasonality in your spending and its effect on your normal spending range

Once you start using control charts to review your spending, there’s no going back. You’ll have a new found sense of confidence and understanding when assessing the financial rhythms of your life.

You’ll rest easy knowing that you’ve got the tools in hand to detect when things are off, and you’ll only spend time investigating issues when it’s actually warranted.

Perhaps best of all though, you’re no longer making decisions by feel. You’re instead using math to make well-informed choices. Choices that can make all the difference when setting out to climb Mt. Savings for instance.

How to start using a control chart

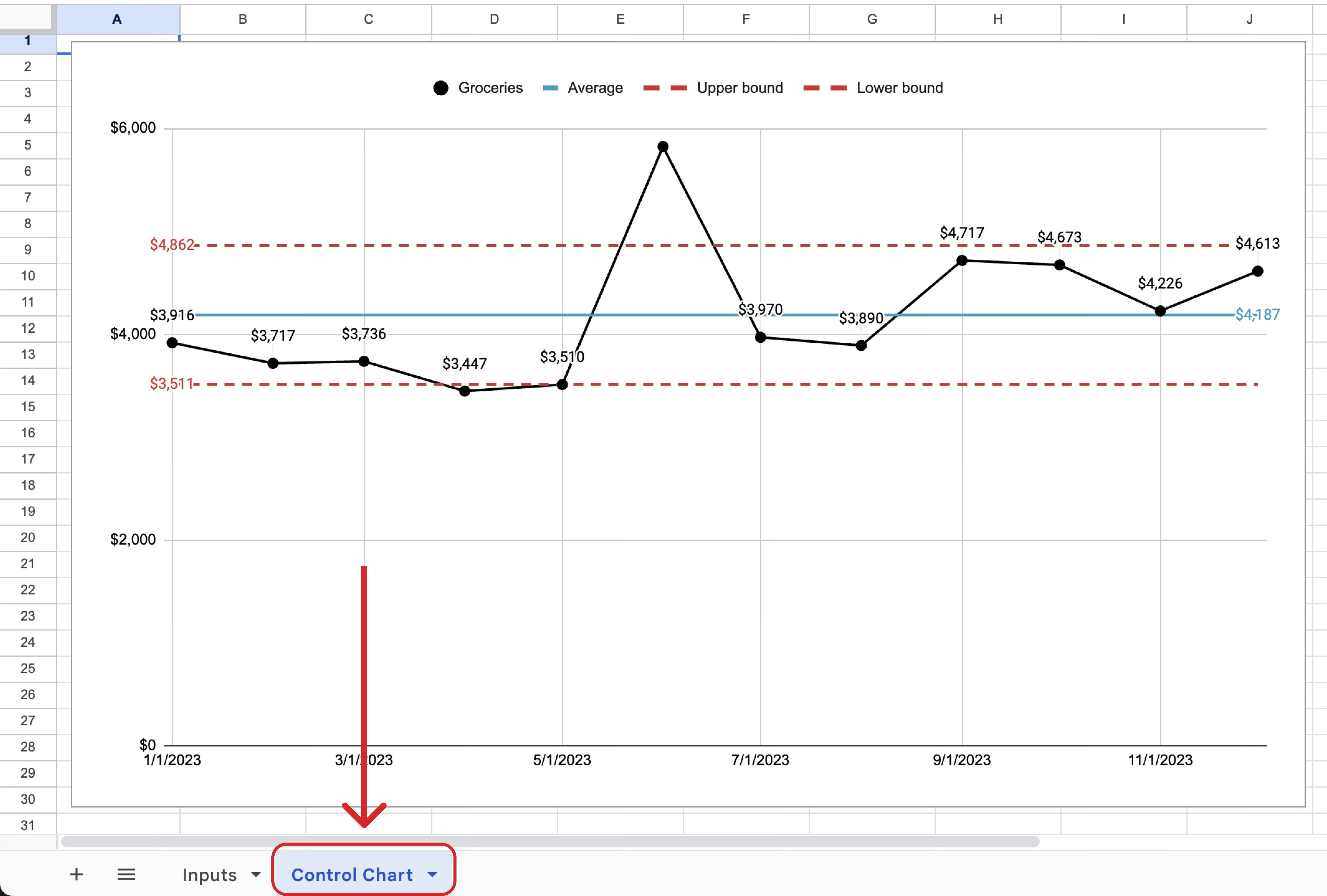

If you’re good with a spreadsheet, building a control chart isn’t too difficult, but it’s a huge undertaking if your first language isn’t Excel.

To make this easy for you, I’ve done the work and created the Control Chart Calculator.

It’s a free Google sheet you can use to quickly create any control chart you’d like. Seriously, it takes less than 5 minutes.

Just follow these steps to get started:

Pick a budget category you’d like to look into.

Pro tip: I highly recommend organizing your budget using the standard budget categories groups.

Pull a monthly spending report for the last 12 months for that category.

Make a copy of the Control Chart Calculator

Key the values from step 2 into the Input tab

Poof! Your chart will be waiting for you on the Control Chart tab

With the power of the control chart in hand, you’ve got what you need to intelligently interpret your spending patterns and set realistic savings plans. Be sure to send me a photo from the top of Mt. Savings when you get there! 🗻