If retirement had to cover your life today

Knowing where you’re headed is half the battle

The topic of retirement is scary. Most of us have no idea how much we should be aiming for, and just about the only thing we’re certain of is that we’re behind. Getting clarity on how much we need and by when either means paying a financial advisor or sifting through a zillion scary online articles that just make you feel even worse. Just like how it’s only a matter of time before WebMD tells you that you have cancer, it’s only a matter of time before finance websites tell you that you’ll die broke.

Enter the 4% rule. This is a practical rule of thumb that’s widely recognized as a great starting point for estimating the amount of money you’ll need upon retiring. The rule states that your money is highly likely to last 30 years if you withdraw at most 4% of your retirement balance in your first year of retirement. In subsequent years, you stick to that rough amount with adjustments for inflation. The rule can be further tweaked to account for periods longer than 30 years if you plan to live a long time, or if you’re looking to retire early.

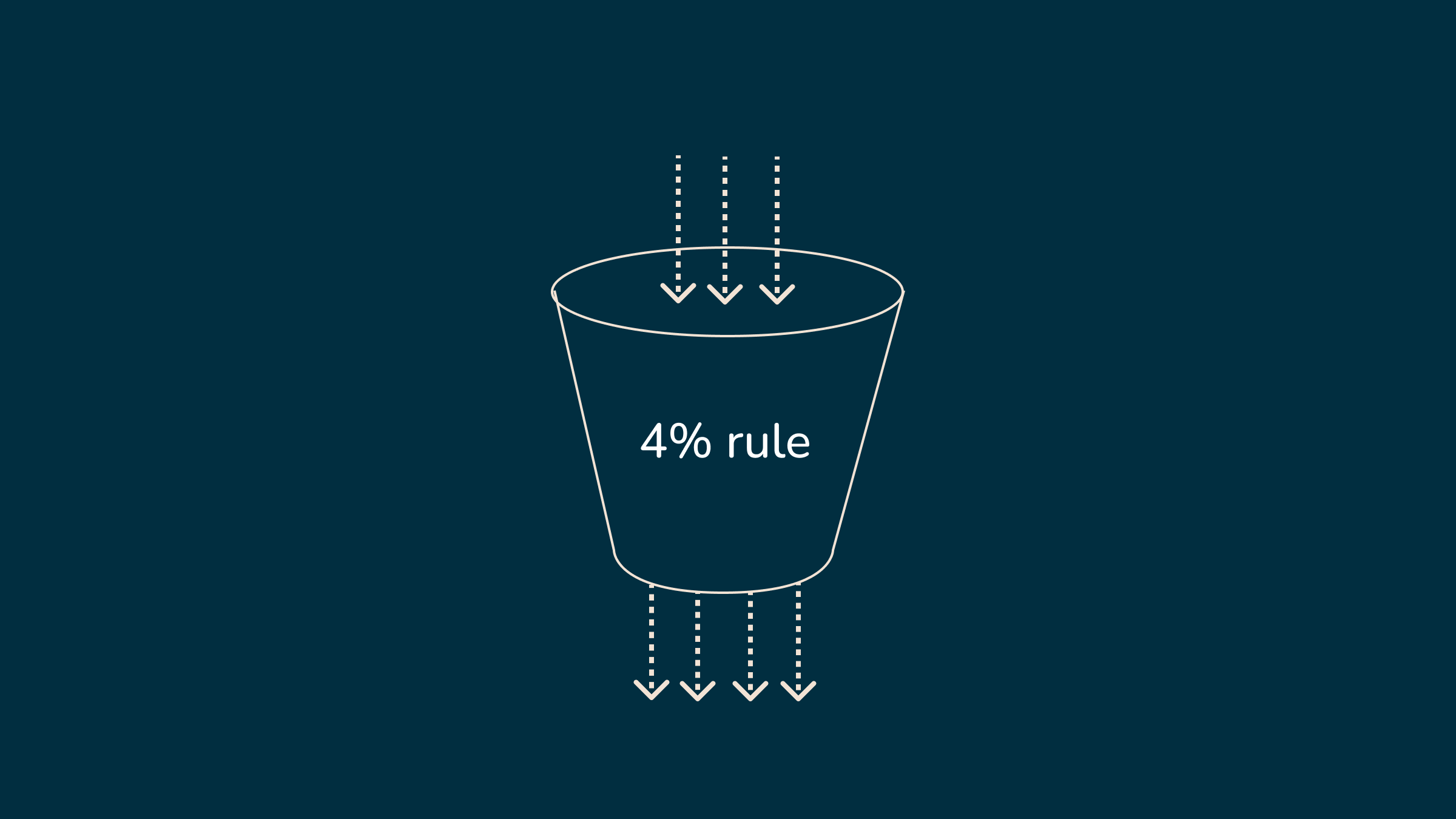

The 4% rule reminds me of a bucket of water that’s slowly leaking, while also getting filled at a slightly slower rate. The typical growth of the stock market represents the filling, while the 4% withdrawal rate represents the leak.

Keep in mind, this is a simple calculation. It doesn’t take into account Social Security, inflation, or taxes, but it does let you know if you’re at least headed to the right ballpark.

To get a feel for how it works, I think it’s helpful to figure out how much money a fictitious retirement account would need to cover your current lifestyle for the next 30 years. To figure that out, take your total spending over the past twelve months (bank statements are helpful for this), and divide it by 0.04.

According to the American Bureau of Labor and Statistics, the typical American household spends roughly $67,000 a year. Divide that amount by 0.04, and you get $1,675,000. That’s a large sum, but before you get scared by it, remember that many of us have time on our side.

With your current lifestyle sized up by a corresponding retirement balance, you can use a retirement calculator to figure out what the journey to retirement looks like. I like this one. Just key in a few numbers, like your age, starting balance, and your estimated annual interest rate (I use 8% in all my calculations) and see what it spits out.

The table below lists the average retirement account balance by age in the United States and the monthly contribution needed to get to roughly $1,675,000. The sooner you get started the better, but you’re still in the game even into your 50s.

The 4% rule is not a replacement for a good financial advisor, but it can help you wrap your mind around whether or not you’re headed in a good direction.

Anytime I’ve started a new job, determining the amount to contribute to a 401k is always one of the first things I need to do. Until I found the 4% rule, this question always felt super hand-wavy. Now, I have certainty on how much I should dial in and can confidently live off the remainder that hits my checking account.