Never be overwhelmed by your money again

Demystify your finances with two simple concepts

For most of my early adult years, my relationship to money could be summed up in one word: denial.

Overdraft fees, never paying my credit card in full, and a constant nagging feeling things would never get better was enough to make me bury my head in the sand.

Once I settled into a career and began earning more, my denial was replaced with confusion. I finally had the ability to save, but I didn’t know when to do what.

Should I build savings or start investing in stocks? Should I max out my retirement, or is it better to begin pulling together a down payment for a home? Do I even want a home?

Then there was my mid- to late 30’s, a time marked by extreme volatility. I was laid off five times over the course of four years. This was a long period of feast and famine that was all about survival.

Though I couldn’t see it at the time, these brutal years transformed me. They forced me how to deeply understand my financial health.

When you never know if your last paycheck is your last paycheck, you get very good at preparing for the worst case scenario. Each time I found myself in financial free fall, I got better at determining how long I had until I’d hit the ground.

After writing dozens of posts about all the challenges I’ve had with money, from my earliest days as an adult through my late 30’s, I came to realize they all stemmed from same root problem.

The underlying issue

All my frustrations, fears, and insecurities around money came from the fact that I simply didn’t know how to make sense of my finances.

I was swimming in datapoints and advice, but I couldn’t clearly summarize my financial health. Was I good shape or not? How worried should I be at any given time?

Once I realized this, I began to see how my lack of understanding provided the fertile ground for all my negative emotions to flourish.

I’d worry that things were extremely bad and dread the thought of being proven right. Ignorance wasn’t bliss. It was stress.

Since I didn’t know how to wrap my mind around my finances, I couldn’t possibly know how to start turning things around. I knew that ideas like saving, investing, retirement, and budgeting all had their place, but I didn’t know which to start with.

Add it all up, and I was left feeling overwhelmed and paralyzed. I’d feel all the stress and anxiety around money, and at the same time, I couldn’t get out of my own way to begin making meaningful change.

All of this frustration motivated a years-long personal finance journey that turned into a mild obsession. I read at least a dozen books, and I dabbled and experimented with budgeting, forecasting, and eventually, even investing.

There was a ton of trial and error before I figured out what worked. For instance, having a healthy 401k balance did nothing for me when I lost my job with only two months worth of savings in the bank.

After accumulating enough scar tissue, I concluded that if you want to turn your financial life around, there is a correct order to the steps to take.

It all begins with step one: You first have to understand how to read and interpret a financial situation.

And the best way to understand any financial situation is to look at it like flying an airplane. Let me explain…

Let’s simplify

Pretend for a moment that you're the pilot of an airplane. There are an infinite number of datapoints to get overwhelmed by, but you only really need to know two things: your height from the ground and whether you're climbing, diving, or flying level.

The same is true for your money. The amount of savings you have represents your height from the ground. Having zero savings and going broke is crashing the plane.

Your monthly cash flow represents your climb rate. If more money comes in than goes out, your airplane is climbing. If more money leaves than comes in, you’re diving. If all the money that leaves matches what came in, you’re flying level.

Every person's financial situation, including yours, can be simplified into these two fundamental concepts. It applies as equally to billionaires as it does to people scraping to get by.

When you start looking at money this way, you begin to realize that there are six situations that help you understand how to size your your financial health. Let's go over them from least to most desirable.

The Six Situations

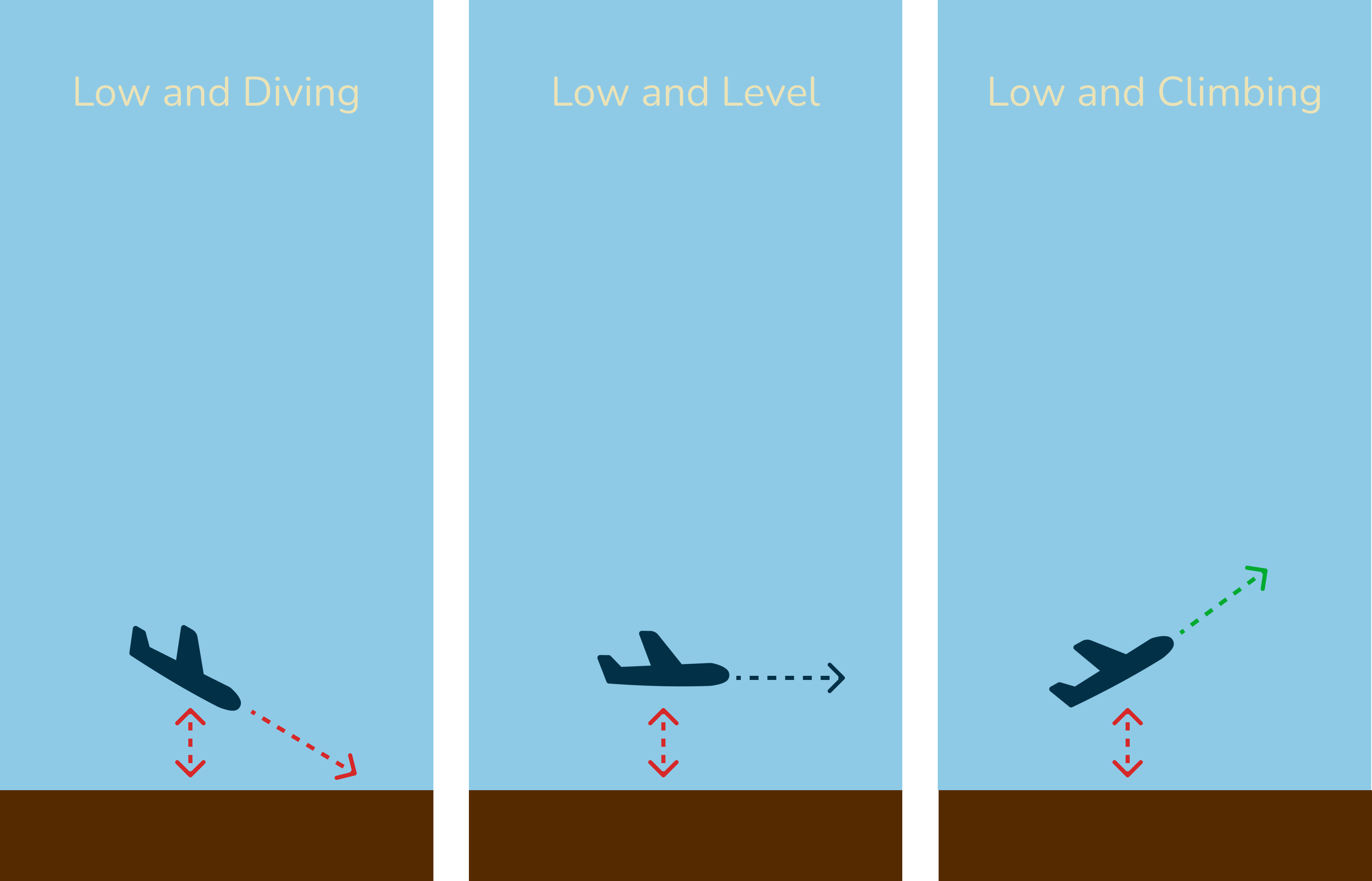

Flying low and diving

This is what it looks like just before you go broke. You’re flying low to the ground because you have little savings. You’re diving because you’re spending more than you make, which is fundamentally unsustainable.

Unless something changes, and fast, it’s only a short matter of time until you max out your credit cards, get trapped by payday loans, and declare bankruptcy.

Flying low and level

This scenario is only slightly better than Low and Diving. This is what living paycheck to paycheck looks (and feels) like.

Since you’re so low to the ground (i.e. have little savings), any slight shift in the wind (a large unexpected expense) is all it takes to put you into a dive and cause a crash.

You’re never far from winding up in the horror scenario above. Your days are filled with tension, stress, and anxiety about money.

Flying low and climbing

While you're still flying dangerously low (I kept that arrow red for a reason), at least you have the ability to reach safer heights. Brighter days are ahead, as long as you don’t squander the ‘extra’ money on frivolous expenses.

Now let’s look at the other side of the spectrum.

Flying high and diving

You’re flying high because you have ample savings, but you’re diving because your income has shrunk. Maybe you lost your job or took a sabbatical. Not ideal, but there's plenty of time to level out and recover.

Flying high and level

You’re flying level because all the money that comes in is going out. Unlike living paycheck to paycheck however, there’s no danger in sight. This is what it could look like when you trade a high paying job you hate for a low paying one you love.

There is a risk in not being able to climb however. Any large expense that takes a chunk out of your savings ends up lowering your height and keeping you there.

Flying high and climbing

This is the most desirable situation and what people think of as being ‘wealthy.’ More money than you need is coming in, and you find yourself with the enviable problem of figuring out what to do with the excess.

You can easily walk away from a job. You can choose to start investing. Imagine the feeling of giving your extra money away to people and causes you want to support.

This kind of flying isn’t only reserved for the wealthy, though. As long as you have enough savings in the bank and spend less than you earn, it’s totally possible to put yourself in this situation.

All other financial situations lie somewhere in between these situations. In the upcoming posts, I’ll be laying out the step-by-step plan to help you figure out exactly where you are and how to get to High and Climbing in the fastest (and safest) way possible.

Better days ahead

Once you realize that your financial situation can be simplified into two, easy to understand concepts (height and climb rate), you’re finally able to act on them.

You’ll feel instant relief at being able to clearly articulate exactly where you stand. When you know your height and climb rate, you exit a distorted world created by your fears and worries about money and enter a new reality grounded in objective truth.

Knowing that you only need to know your height and climb rate instantly delivers a sense of calm because you can now easily see which problem to tackle first (gaining height or increasing climb). Your mind is no longer spinning in all directions. You know where to focus.

When I noticed this for myself, I begin to feel a genuine sense of hope because I could finally see a clear and easy to understand path for getting my plane to soar above the clouds.

Perhaps best of all, this simple foundation will allow you to make sense of how and when to do all of those overwhelming and confusing things like saving, paying down debt, and investing.

When it comes to the basics, you are your best financial advisor. All you need is the right information presented the right way.

Shake the rust off

If you haven’t exactly been on top of your finances for a while, don’t fret. It’s never too late to reengage, and there’s no better time to start than now.

While we will go into detail about how to calculate your precise climb rate and height in the next post, there are a few warm up exercises you can do now that will make the next steps easier to complete.

1. Log into all your financial websites

It might have been a while since you last logged into the websites for your checking and savings accounts, credit cards, and other debts like student loans or mortgages.

Now’s a good time to find those website addresses and reset any passwords that you might have forgotten. Make bookmarks and track your passwords in a secure place. I’ve been a happy 1Password user for over a decade.

2. Note the balances

As you reacquaint yourself with your financial life, log the balances of all these accounts in a notebook or text file. Simply writing these numbers down will kickstart a relationship with them.

We’ll eventually work with each of these numbers, but for now all we’re doing is figuring out what’s what.

3. Reflect and resolve to change

Over the years, especially in the beginning, I lost count of how many times I set out to ‘straighten out my finances.’ I’d always start off strong (usually on January 1st) and lose steam by March. I struggled to keep my motivation and spirits high.

The key to eventually breaking through and finally making lasting, permanent progress was getting real with myself about how unhappy I was.

Taking a page from the world of habit formation and behavior change (another deep interest of mine), I journaled about my feelings around money. I didn’t hold back.

In the moment, getting all my thoughts out of my head felt like removing a huge weight off my chest. Not only that, but re-reading those same thoughts in later months always served as a potent reminder of how far I had come and what was left to look forward to.

Given my experience, I highly recommend taking an hour and journaling about the following questions:

Write down your best guess at how you think your ‘financial airplane’ looks. How far from the ground does it feel like you’re currently flying? Do you think your climbing, diving, or flying level?

Read what you just wrote and write down how those words make you feel. Get really detailed and don’t hold back.

Describe what it’ll look like when you’re flying high. What will you be able to start doing? What will you be able to stop doing? Again, be specific.

Now that you’ve got a framework to interpret any given financial situation, it’s time to actually figure out your specific numbers. That’ll be the focus of the next post.

If you’ve received value from this article, please be sure to subscribe. You’ll instantly get notified when the next post is published, and you’ll be helping me grow my newsletter. Win win.

Thanks for reading, and I’ll see you in the next one.